-

The benchmark for these highly litigated home loans is no longer published

There is no rest for those affected by multi-currency mortgages. Those who took out a loan years ago to buy a home in currencies other than the euro, and thought they were going to save money, were swallowed up by a growing debt caused by the devaluation of the euro. According to estimates by Asufin, an association of consumers of financial products, there are 70,000 multi-currency loans in Spain: 52% indexed in Swiss francs, another 46% in yen and the remaining 2% in pounds and dollars.

As they recall from Asufin, “there are ongoing lawsuits from affected customers of all banks” who have marketed these products, claiming a lack of transparency, insufficient information… In 2017, the Supreme Court annulled one of the multi-currency clauses declared and the entity that issued the loan (Barclays Bank) forced to recalculate it as if it had been granted in euro and repaid and referred to the Euribor. Since then “all sentences are won”, say Loleta Linares, CEO of Gavín y Linares and associate lawyer of Asufin, but there are still many open processes to which another front is now being added: the disappearance of libor. This index serves as a reference for multicurrency and above all in variable interest rates. On 31 December 2021, Libor ceased to be published in all its currencies (euro, Swiss franc, pound sterling and yen) and terms, with the exception of Libor in dollars, which will be published until June 2023.

The result? According to the Bank of Spain on its website, “these mortgages they will lose the reference to calculate the interest rate to be applied in the periodic review and therefore quotas can not be determined. “

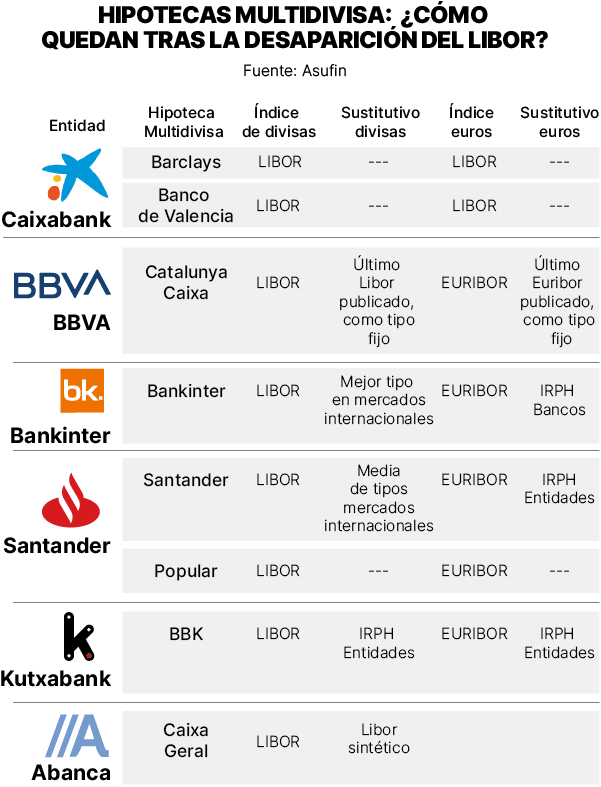

In some cases, the situation is provided in the deeds as a substitute index is established, but this is not the case in all signed mortgages. And banks and customers have caught up. Sources from Arriaga Asociados acknowledge that inquiries about various currencies have increased and ensure that, “in general, the entities have communicated possible alternatives or solutions very late.” At this point it coincides Miquel Rieraresponsible for mortgages at HelpMyCash: “We know the entities were slow to respond”.

One of those who did act beforehand was CaixaBank. The Catalan bank has announced that the change will be made with a new contract, which could close the doors for a future claim, and that it includes an early expiration clause. “He first tried to scare his customers with this risk, but days before 31 December he retreated and found a way to calculate the interest with the last rate applied ”, they say of Arriaga.

Other entities, such as KutxaBank, consider the IRPH to be a substitute index, which has been declared abusive in many courts. “We fight it a lot, but it’s official because it’s published by the Bank of Spain,” Linares complains.

Bankinter, which endorsed about 50% of these bonds, and Banco Santander chose to take advantage of what the European authorities state. And for now, what the European Commission has done is to issue a regulation with the SARON (Swiss average rate overnight) index, the Swiss average rate, as a regulatory substitute for loans referred to in Swiss francs. For those referred to in yen, no statement has been made yet, although it has been decided that a synthetic libor will be published for the time being, with a different calculation formula, until December 2022.

attention to February

If a multi-currency bond provides for a specific index or alternative rate, from Arriaga Asociados they confirm that “the logical thing” would be for the bank to use it and “there will be no problem”. “The problem will come if the bank and the customer have not reached an agreement or solution ”, warns them.

Related news

The affected person who finds himself in this situation should be “very attentive” to the fee transferred to him in February, “because that is when they are going to apply the new index or what is agreed upon,” Linares recommends. which defines these mortgages as “the most abusive and toxic financial product we have known in the 20 years we have been with the firm”. In January it was still paid with the December libor as reference, so it will be in February when it will be possible to know which way the entity is heading. Asufin also recommends no novation sign which could have been proposed: “It is not necessary to accept these contracts, because it complicates the lawsuit with many currencies,” he defends Patricia Suarezpresident of the association.

And in the event that negotiations are still pending, the HelpMyCash mortgage manager believes that on paper would be the most appropriate option to replace the libor with the euribor, which is trading below 0% (-0.502% in December 2021). “Applying a fixed rate equal to the last interest rate applied would also be a good solution if it is low; 1.50% or less,” Riera adds.

Reference-www.elperiodico.com