Related news

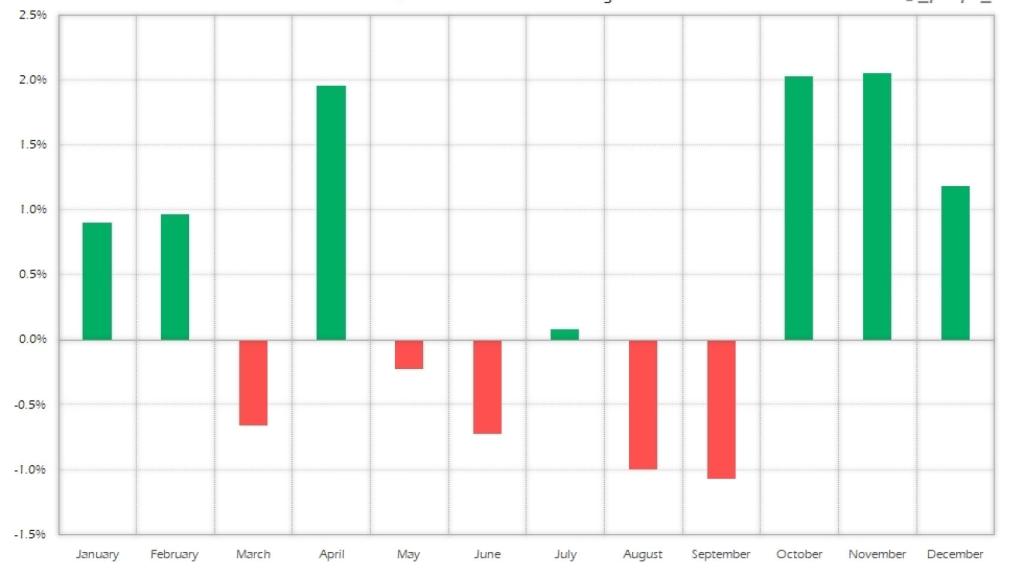

The statistic is clear: September is the only month that, on average of 10, 20 and 70 years, has a negative return for the main world stock index: el S&P500. And to that we must add that it also tends to drop in the year immediately after a presidential election.

Nevertheless October, which has such a bad reputation since crash of 1929, it is a month, contrary to what many think, that it turns out positive on average taking different time parameters.

However, although it is striking that a month is on average bearish, we are talking about a percentage of fall that only in the case of the year after the elections – just the current one – exceeds 1%, the rest are almost testimonial assignments.

AND if this year the statistics were fulfilled and Wall Street will go down, taking into account the cumulative rise and the recent all-time highs, it would hardly be a correction that would not change the trend, even if you multiplied the usual average drop for the month by several digits.

Another topic would be Ibex, which is not in as good a technical condition as the US stock indices.

Why does this pattern occur

There are guidelines that have a certain “logical” explanation such as the one that determines that the first day of the month the probability that the stock market rises is higher. It seems that this is due to the fact that they are dates with greater flows of money to potential investors. The same happens with the first half of January, which is when most decide to make more investments.

Others are assumed, such as those that indicate that the weeks after futures and options expire tend to be more downward Due to the fact that, as most of the major players in the markets are invested, there is a certain upward manipulation during the week and, above all, on the Friday of maturities, an effect that disappears the following week.

However, there are others that no one can explain why they occur. Last week, for example, we explained here that a seasonal guideline had been activated that says it is a good idea to sell on the Jewish New Year, Rosh Hashana, celebrating renewal, and buy back in the Yom Kipur, the holiest day on the Jewish calendar.

It is a period of ten days of much spirituality and reflection for the Jews who undo their portfolio of values during the same. The effect of these sales on the market explained some important falls in Wall Street in the 20s and 30s of the 20th century, when the depth of the market was less than now.

And we explained that, although the reason is so old, the pattern is still in force according to statistics since in the last 50 years more than half of the time the Dow Jones it has fallen in that period when, most of the time, this index rises.

And this year it seems that it is fulfilled, since it began on September 6 and will end on September 16 and, for now, since May it did not happen that the S & P500 did not drop 5 consecutive sessions as it happened last week.

There does not seem to be a logical reason for that pattern to work since global financial markets are large enough that a Jewish holiday cannot influence them but… it happens. We can still think of September: perhaps it is simply fulfilled because most believe that it will be fulfilled.

“Rational” reasons

Making it clear that the stock market trend is bullish, it is true that many arguments are accumulating to justify the stock market corrections, beyond the purely seasonal ones.

The clearest is that the stock market takes expectations into account And these are that the maximum point of stimulus from central banks is close to ending, so liquidity in the system will grow at a slower rate until it stops increasing, as a first step so that in the future, still distant, reduce.

This is motivated by a rising inflation that, although transitory, is greater than anticipated and, surely, more durable than expected. If the reason were exclusively higher consumption, and therefore higher growth, it would not influence the listed companies. But there are other factors.

Energy prices are very expensive, there are supply problems across various industries, and the price of their transportation is skyrocketing as well. There’s a rising prices for the final consumer that goes from the house to the gasoline going through the own shopping basket. And to all that is added a tax increase almost widespread.

Xi Jimping has started a campaign against the Chinese stock marketDifficult to understand from a Western point of view, it has caused a sharp correction in its stock indices: it went against Jack Ma, the founder of Alibaba, and the stock plummeted; he legislated against private academies and also plunged their contributions; regulated that children could only play video games online three hours at the week; and it generated a wave of sales in the companies of the sector, including Tencent.

He also does not seem willing to rescue Evergrande, on the verge of bankruptcy. AND, as everything is related to the markets, influences in some way. Nor can we forget that Covid it is still there, with the risk of a new variant even worse than the Delta.

The German elections on September 26 (which, by the way, are associated with a bearish pattern that is activated two weeks before each election in Germany) or political discussions in USA by the need to agree on a new debt ceiling and a possible tax increase, are reasons for uncertainty as well.

On the other hand, many indices and stocks trade very close to highs of many years (in the case of the Euro Stoxx50 or the Nikkei, for example) or very close to all-time highs (such as Wall Street and the Dax).

We saw it last Friday with Apple, the value with the highest capitalization of the New York Stock Exchange, which fell 3.3% (its biggest fall in four months) due to a judicial setback, although it is still trading at less than 5% of its all-time highs. A more significant correction would hardly mean anything to a security with such accumulated returns.

With everything, the biggest risk is complacency. After the strong rebound after the shortest downtrend -in 2020- in history on Wall Street, the idea that the market, although it may have specific corrections, can only go up.

Even the seasonal pattern argument makes it clear that even though September is bearish, the last quarter is the best of all for the stock market. In other words, only a correction is contemplated but not a change in trend.

The case of the Ibex

To the Ibex much of the “economic” bearish arguments apply to it since although GDP rebounds strongly after the collapse of 2020, we are still not close to returning to the pre-pandemic level, inflation is very high, public accounts are not doing well, the political environment is not very stable …

And yet it is difficult to apply the maxim of the high valuation of our listed companies or of the great complacency.

Quite the contrary, the Spanish type investor, although this is a positive year, it is in a more fatalistic than optimistic phase, and many securities, by classical valuation criteria, are not “expensive.”

The Ibex weakness, demonstrated in recent weeks by being unable to recover the 9,000 points, is very clear. Nothing to do with the atmosphere of euphoria in investors, for example, the Nasdaq.

The loss of supports last week of the most weighted security in the index, Iberdrola, is a worrying sign for the short term.

However, if we trust seasonality (although it failed in August since this year it rose against usual), the last quarter predicts a good annual result that may bring it closer to the returns of other European stocks That, in the case of the Euro Stoxx50 or the French Cac, today more than double the Ibex in percentage revaluation so far in 2021.

Let’s hope we are not falling into the excessive complacency we mentioned earlier.

Follow the topics that interest you

Reference-www.elespanol.com