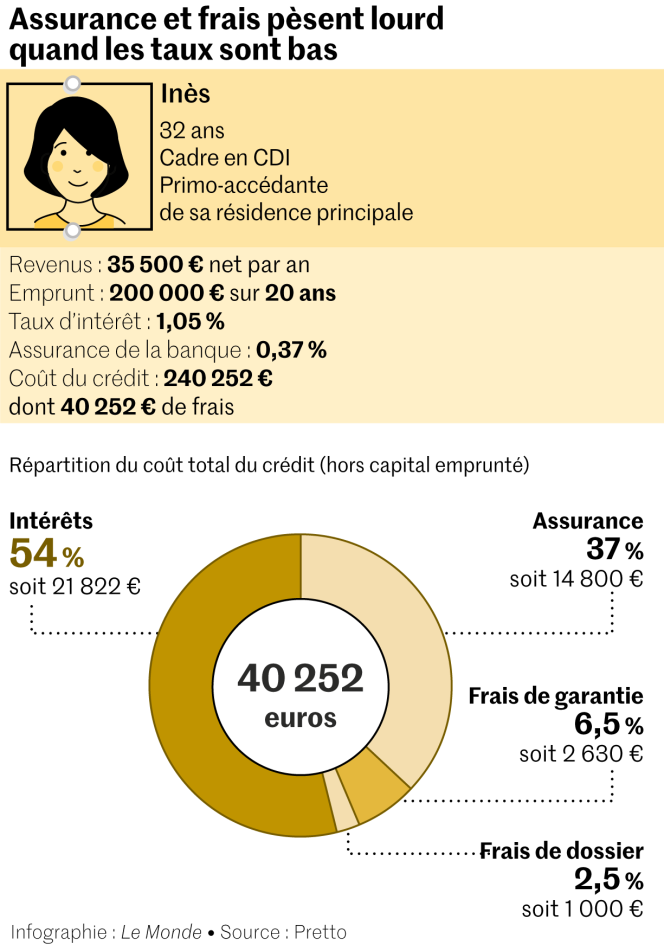

Borrowers are all looking for the best rate for their loan, and this quest for the Holy Grail can make them forget another item that will weigh heavily in their future monthly mortgage payments: insurance.

However, this insurance, which must reimburse all or part of the loan for you in the event of temporary incapacity for work, permanent disability, total and irreversible loss of autonomy (PTIA) or death, often represents 40 % of the total cost of the loan. Sometimes even more than half. The cost varies according to the risk profile of the purchaser (age, state of health), the guarantees chosen and the insurer.

Most borrowers take out loan insurance offered by the bank granting them the credit. But these group contracts are expensive, billed between 0.30% and 0.50%. You can significantly reduce the bill by delegating insurance, that is to say by taking out an individual contract with an external company offering guarantees equivalent to those of the contract offered by your bank.

“The delegation makes it possible to obtain a rate of between 0.08% and 0.20% for 25-45 year olds. The borrower can thus save several thousand euros ”, indicates Antoine Fruchard, founder of the broker Reassure me.

Despite everything, the delegation remains in the minority, under pressure from the banks which are protecting their share of the pie. “Some require the subscription of their group insurance to grant the loan, others increase the interest rate if the client requests a delegation”, explains a broker.

Do not insist

However, regulations facilitate competition: the borrower can not only delegate his loan insurance to the subscription of it, but also change borrower insurance at any time before the first anniversary of the credit. A right that he can still exercise after the first twelve months, but once a year, on the anniversary date of the loan. Some advocate that borrower insurance can be canceled at any time, even after the first year, as with home and auto insurance.

In practice ? The subject must be discussed with the bank from the start of the negotiation. If you indicate to her your wish to take out insurance in delegation, with a supporting quote, she will sometimes make you a counter-proposal. She will then direct you not to her group contract, but to an individual in-house contract, which is less expensive. “But if she is reluctant, it is better not to insist, there will always be time to change after obtaining the credit”, advises Clarisse Loobuyck, Marketing Director of Magnolia.fr.

You have 41.76% of this article to read. The rest is for subscribers only.

www.lemonde.fr