-

Families only accumulate 74,000 million euros in these financial products

The financial sector is minimizing the interest at which families’ fixed-rate deposits are remunerated, so that it is impossible to find in them a refuge from the escalation of current inflation. Due to this, depositors are betting less and less on this type of investment, as has been seen in the data of the last decade. In 2021 alone, they reduced their deposits by 27% to 78.3 billion euros, according to data from the Bank of Spain. This represented a historical minimum, after the maximum peak that occurred in 2013, with 415,470 million. Currently, the figure has already fallen to 73.9 billion, according to the latest data.

Specifically, the average interest on fixed terms is 0.01% up to one year, 0.22% between one and two years and 0.04% on those held for more than two years. These are “incapable” of protecting the capital from the increase in prices, which rose 9.8% in March, explains olivia feldman, HelpMyCash spokesperson. That is, even if you invest in them, you are still losing money due to the general increase in the cost of living.

The low interest rates are due, in part, to the ultra lax monetary policy of the European Central Bank (ECB), which means that banks “no longer need their clients’ deposits to obtain liquidity”, as explained Antonio Gallardo, Banqmi expert, iAhorro’s financial comparator. The situation already started in 2012, when the banks solved their need to capture a lot of money due to the financial crisis. In addition, since 2018 normal returns range between 0% and 0.1%.

“Everything that is not risky is at a loss. Even many risky products are not capable of beating inflation,” says the Banqmi expert. “To start seeing interesting products, inflation would have to be at least below 5%,” he specifies. Gallant.

It is worth mentioning that the European financial sector has had a negative deposit facility for seven years, which fell to -0.5% at the end of 2019, and that analysts do not expect it to change for a while. The deposit facility determines the interest that credit institutions receive for having the money parked in the central bank, but once it is below zero, they have to pay for the excess liquidity deposited. “As long as that guy doesn’t move, there will be no stimulus from the banks to vary the remuneration of deposits,” according to Henry Raindirector of fixed income at Imantia.

The rate hikes expected by the central banks would, however, be favourable. “Rises in interest rates are expected, but this will take time to spread throughout the financial system and, even so, we will surely not see large increases,” he points out. Monica PineCEO of Raisin Spain.

Despite this situation, then why are there still people who keep their money in fixed-term deposits? “Spain is very conservative in saving. It is preferred not to earn money to risk losing it and that is why there is little movement towards investment funds. There is a lack of financial culture,” he explains. Antonio Gallardo. Therefore, it is especially important for Spanish savers to be proactive when looking for attractive ways to save, both to put their capital to work and to be prepared when these policy changes occur.

Where are there good deals?

Related news

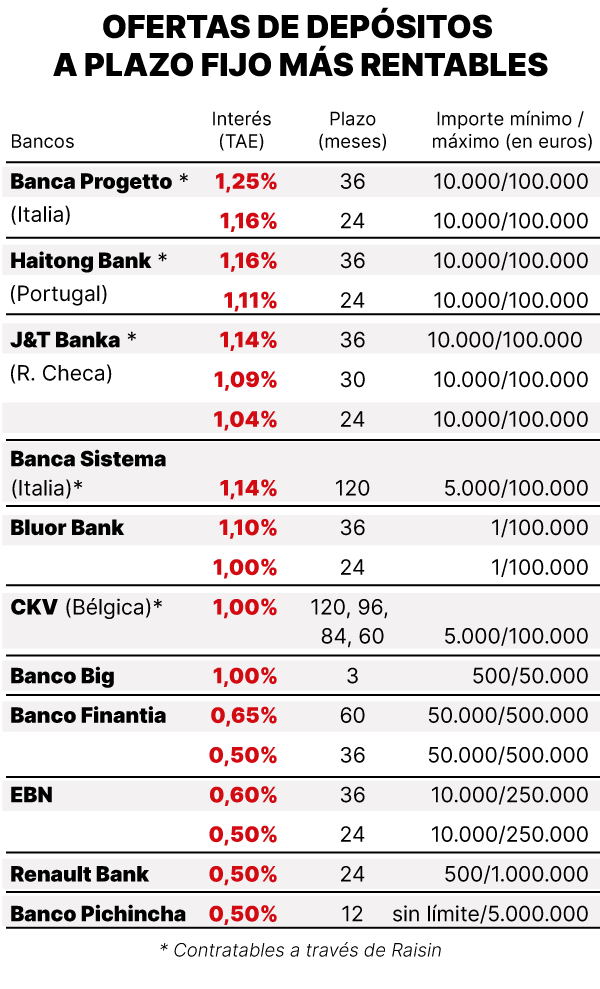

However, there are above-average products on the market, such as those offered by European banks with specialized business models that require short-term liquidity, which are marketed through platforms such as Raisin. In that application you can find an annual equivalent rate (APR) of up to 1.25% for 36 months in Banca Progetto (Italy). At the same term, the Portuguese Haitong offers 1.16%; J&T Banka (Czech Republic) 1.14% and Bluor Bank 1.10%.

In addition, while the big banks flee from high interest rates, there are also other medium and small digital ones in Spain that promote them. “WiZink offers deposits to capture liquidity to market credit cards, while Renault Bank does it to be able to finance cars. Big Bank, for its part, offers higher returns to be able to later offer investment products. Others are probably simply looking for make themselves known,” he explains. Pineapple. The investor has very few options because inflation is covering everything, experts conclude.