These two years have been characterized by the presence of the pandemic, which certainly generated some disruption in some value chains and has had an impact on the costs of certain inputs; we import the volatility of prices derived from conditions in the international environment and are not specific to the grain or fertilizer market, as mentioned by Alan Elizondo Flores, CEO of Trusts Instituted in Relation to Agriculture (FIRA).

In an interview with The Economist, Elizondo said that 2020 was the most complex year because it was coupled with a very strong liquidity astringency in the financial markets, which even reached the banking market.

“As a second-floor entity, we live it in the front row, especially in the context of a second quarter in which, public debt markets they dried up, that quarter the placement was minimal and the demand for credit, on the contrary, was higher than normal. We perceive that this higher demand was due to issues of risk aversion both companies and financial intermediaries “, considered the manager.

FAIR It has tried as a policy to stay present and not only that, where a source of liquidity for the primary sector has been lacking, they have cushioned and even made that lack of liquidity in the market imperceptible.

Operation with UC

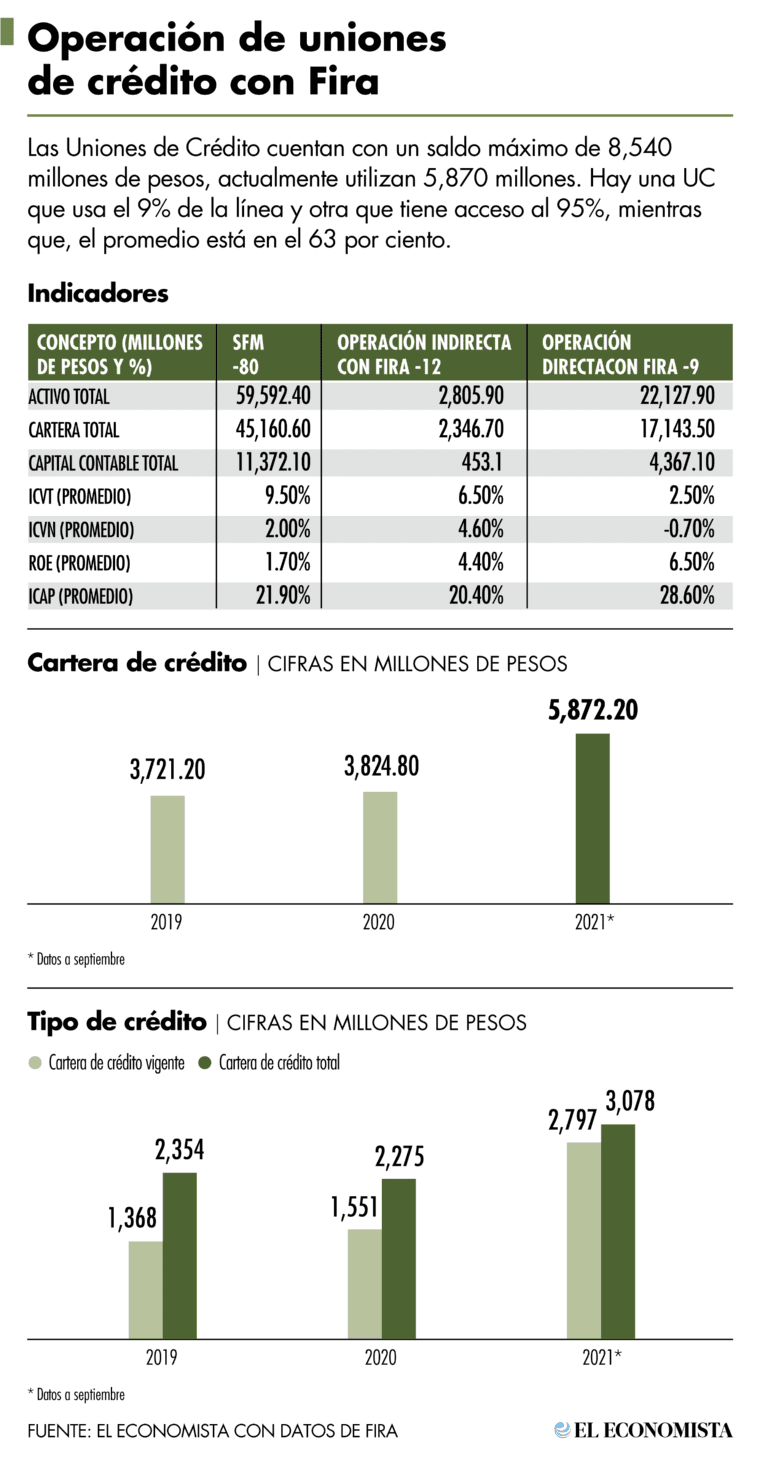

The market has around 80 Credit Unions that report information to the National Banking and Securities Commission (CNBV), FIRA operates with 21 UC, 12 of them in indirect operation and nine in direct operation.

“The total assets of the 21 UCs add up to around 25,000 million pesos, the total assets of the 80 UCs stand at 60,000 million, which means that we have a 40% presence in the market, specialized in UC of the agro-industrial sector, milk producers (Alpura and Lala).

“We have the large grain producers in the north of the country, such as the Cuauhtémoc farmers. We have further opened our network to some UC with an indirect association such as UNICCO.

“We like to operate with entities that are highly specialized and regional, such as the Tabasco Livestock, the UCEPCO that has an interesting presence in the coffee chain ”.

Elizondo considered that they are happy with the network they operate, since they have a record balance with the UC of 5,872 million pesos of balance.

“We see very controlled levels of overdue portfolio, the lowest brings 0%, the highest brings 3.0-3.1% and if you consider the provisions to deal with it, the exposure to risk is practically at 0, in that sense we are comfortable with the operation “, said.

Actions

In 2020, they launched a package to address the conditions of the pandemic, although the primary sector remained essential, “there were no drops in the production part, perhaps a little in the marketing chain or in the services there were damages, therefore they facilitated credit restructuring ”, explained the FIRA executive.

He said that 182 million pesos of credit were restructured that went to longer-term conditions, “and those who had some type of problem we endowed them with 225 million pesos of additional credit, the FIRA package included other facilities, but both that we observed with the UC were restructures and additional credit so that the activities of these companies did not collapse ”.

Warranty product and others

Elizondo explained that there are certain producers who are less consolidated and who cannot give a guarantee, a collateral, perhaps they do not have that number of hectares that the UC asks for as collateral for credit or there is a doubt in the credit profile and there are two decisions to give or not to give the financing, typically the entities choose not to give the credit.

“We offer a guarantee, it is like insurance, we give UC the certainty that if the producer defaults, FAIR pays 50% of the balance, half of the risk belongs to the government, “he said.

The warranty product is an old product in the drawer. FAIR and covers 50% of the balance, they charge a premium that is more or less than 1.5 percent and is known as COWARDLY.

FAIR opened another financing option through a mutual fund of 10% of the loan, three entities must join that show interest in being accredited.

“We will shortly announce the first Credit Union that joined with a SOFOM and with a SOFIPO, who are looking for alternative channels with fewer requirements ”, he concluded.

patricia.ortega @ eleconomista.mx

rrg

Reference-www.eleconomista.com.mx