With the US economy still on fire and inflation galloping, the Fed has to react firmly. What will happen to gold after the dovish stance changes?

It’s a decision day for the Fed as a 50 basis point rate hike is likely to be a given. Furthermore, while PMs may post a short-term relief rally, their medium-term fundamentals continue to deteriorate.

For example, I have been warning for some time that higher interest rates would manifest amid runaway inflation and, surprise, surprise, the 10-year US Treasury yield has continued to rise. Also, while the benchmark Treasury index eclipsed 3% intraday on May 3, a close above the key psychological level should come sooner rather than later.

To explain why, I wrote on April 20:

The red line above follows the US fed funds rate, while the green and gray lines above follow the 10-year and 30-year US Treasury yields. If you analyze the connection, you can see that the latter two often take orders from the former. In one word: when the Fed raises interest rates, it takes several 0.25% hikes before long-term yields renew. For example:

-

In 2018, the 10-year US Treasury yield peaked after ~9 rate hikes.

-

In 2006, the 10-year US Treasury yield peaked after ~17 rate hikes.

-

In 2000, the 10-year US Treasury yield peaked after ~7 rate hikes.

-

In 1994, the 10-year US Treasury yield peaked after ~12 rate hikes.

So, with modern history showing that the 10-year US Treasury yield doesn’t peak until the Fed is inside its rate-hike cycle, remember that the Fed has only gone up once. So, with at least seven rate hikes to spike in the last ~28 years, the 10y US Treasury yield should have room to run, and this is bullish for real yields and bearish for gold.

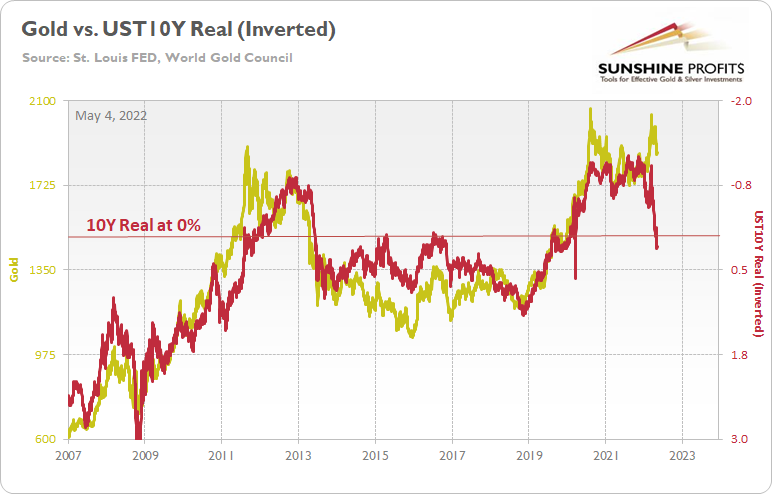

Speaking of real returns, with nominal interest rates rising and implied inflation rates falling, US 10-year real yield closed at 0.18% on May 2 and 0.15% on May 3. As a result, PMs face a fundamental time bomb that should blow up their performance in the coming months.

To explain, the gold line above follows the World Gold Council tally price, while the red line above follows the US 10-year real invested yield. For context, inverted means that the scale of the latter is inverted and that a rising red line represents a fall in the 10-year US real yield, while a falling red line represents a rise in the US 10-year real yield. USA at 10 years.

For more context, I wrote on April 11:

If you look at the left side of the chart, you can see that the real yield on US 10-year bonds soared and gold crashed during the global financial crisis (GFC). However, when the Fed launched QE and the real yield on US 10-year bonds fell to an all-time low, gold hit a new all-time high along the way.

Furthermore, the current situation is a vivid image. When Fed Chairman Jerome Powell pivoted dovishly in late 2018, the real yield on 10-year US bonds suffered. Then, when the Fed fired its liquidity bazooka in March 2020, he took the metric to another all-time low. And surprise, surprise, gold hit another all-time high.

Nevertheless, With the Fed’s policy normalization, the real yield on US 10-year bonds has risen in recent weeks. Also, the Fed needs to push the metric above 0% to curb inflation.

So it is likely only a matter of time until the milestone is achieved. Besides, 0% US 10-year real yield implies a gold price of $1,500and although the current narrative suggests otherwise, is this time really different?

Until then, although gold has suffered in recent days, the current price is still well above its average value based on the trend. Likewise, since the GDXJ ETF is much more volatile than the yellow metal and therefore should decline further, epic drawdowns should materialize if (once) the two lines reconnect (not necessarily immediately after of the rate increase, as PMs could rally based on the trend of moving on the rumor-investing in the fact).

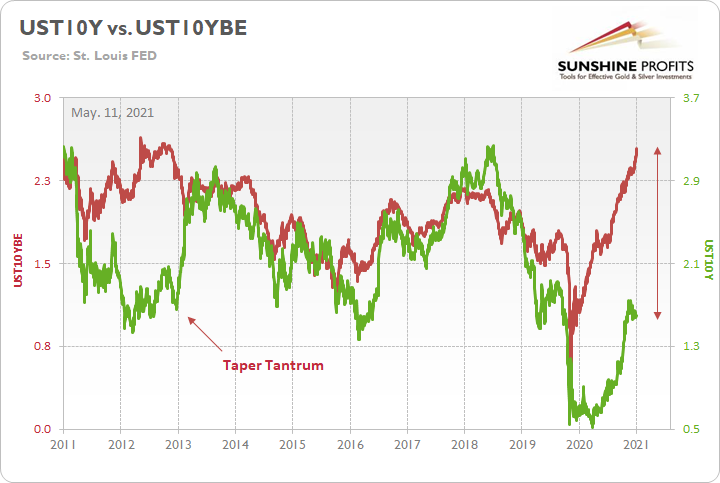

For example, while these events take time to unfold, history shows that the “this time is different” crowd ends up losing more than just their pride. I first highlighted the epic divergence between the 10-year US Treasury yield and the 10-year US equilibrium rate of inflation on May 11, 2021. I wrote:

To explain, the green line above tracks the 10-year US Treasury yield, while the red line above tracks the US 10-year breakeven rate of inflation. If you look at the left side of the chart, you can see that when the bond market finally crashed in 2013, the rise in the 10-year US Treasury yield was fast and furious. More importantly though, if you look at the right side of the chart, you can see that today’s gap makes 2013 look like a snack. As a result, with material divergences often violently reversing, it is only a matter of time until the next earthquake strikes.

Thus, although the fundamental thesis did not materialize overnight, the two lines were eventually reconnected; the 10-year US Treasury yield exceeded the 10-year US equilibrium rate of inflation, and the 10-year US real yield turned positive.

Nevertheless, now it is the gap between gold and the US 10-year real yield that makes 2011 look like an appetizer, and the same result should occur. As a result, the outlook is deeply pessimistic for prime ministers.

from negative to positive

Instead, with bonds oversold and the stock market nearing a breaking point, investors continue to ask, “Where is the Fed?” By context, put options are like insurance contracts and protect investors when drawdowns occur. Bottom line: Investors are hoping the Fed will step in, turn dovish, and save stock market investors from their poor valuation decisions.

However, the perspective is far-fetched, and here’s why. After the global financial crisis (GFC), the Federal Reserve rushed to the rescue every time the stock market threw a tantrum. As such, memory-poor inverters assume the post-GFC script is the correct analog. They fail to realize, however, that the year-over-year (YoY) percentage change in the consumer price index (CPI) peaked at 3.81% in September 2011. So the Fed could relax without worrying. for fueling inflation.

On the contrary, with the headline CPI at ~8.6% YoY now, the game has completely changed.

Second, the other half of the Fed’s dual mandate is maximum employment. With US job openings hitting an all-time high of 11.549 million on May 3 (March results), the data is extremely bullish for Fed policy. For context, the consensus estimate was 11 million.

![]()

Source: Investing.com

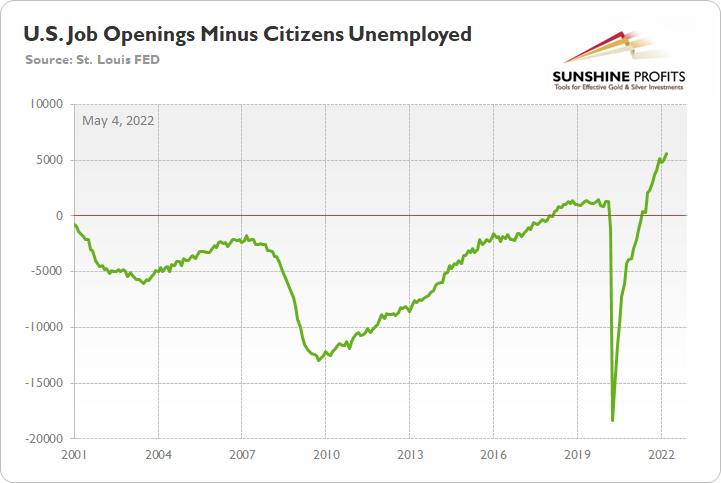

More importantly, however, another resilient report means that there are now 5.597 million more job openings in the US than unemployed citizens, also an all-time high.

To explain, the green line above subtracts the number of unemployed US citizens from the number of job openings in the US. If you look at the right hand side of the graph, you can see that the epic crash has been completely reversed and the green line is at an all-time high. Thus, with more jobs available than people looking for work, the economic environment supports normalization by the Fed.

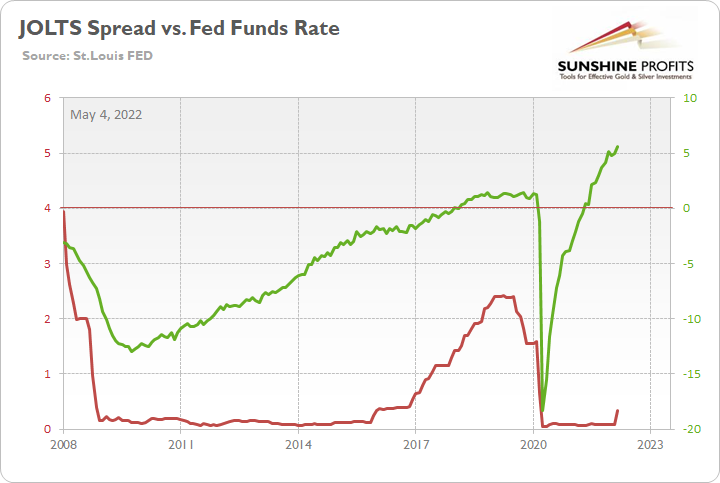

Again, note the CPI data above with job postings distributed after GFC. The period had well-anchored inflation and unemployed citizens outnumbered job openings through 2018. That’s nothing like the current environment. Also, can you notice how the outperformance of the spread helped fuel the Fed’s most recent rate hike cycle?

To explain, the green line above tracks the job offer spread, while the red line above tracks the US fed funds rate. If you analyze the relationship, you can see that the spread’s move toward neutrality was a hard line indicator.

Also, with the positive spread and at all-time highs, the data alone justifies several rate hikes. However, as mentioned, we also have headline CPI year over year that is at its highest level since the 1980s. So if investors assume the Fed lacks ammunition to deliver on its hard-line promises , should suffer the same fate as the “transitional” field in 2021/2022.

Finally, S&P Global released its US Manufacturing PMI on May 2. The report revealed:

“Operating conditions have improved markedly across the US manufacturing sector, according to April PMI data from S&P Global…. New orders rose at a marked pace at the start of the second quarter, and at a pace broadly similar to that seen in March. Companies reported stronger demand conditions, with some noting that new sales expanded despite substantial price increases. Meanwhile, new export orders grew at the fastest rate in nearly a year.”

Also noteworthy:

“Manufacturers posted a solid increase in employment in April. The number of workers increased due to higher production requirements and in response to the voluntary departure of staff. Some companies also claimed that job creation was linked to the filling of long-standing vacancies. Labor shortages continued to be cited as a drag on growth, Nevertheless.”

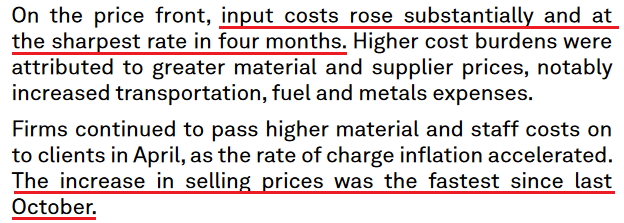

However, what is more important:

Source: S&P Global

The bottom line? While investors continue to pray for a dovish turnaround, they are likely in for a rude awakening. The US labor market remains abnormally active and the latest PMI data shows that inflation continues to accelerate. Furthermore, while real yields have turned positive, they have done little to cool down a US economy that is awash with too much stimulus. As a result, with a hawkish Fed poised to boost real yields on US 10-year bonds even further in the medium term, PMs should suffer badly as the drama unfolds.

In conclusion, PMs rallied on May 3 as sentiment does not die easily. However, while the technical backdrop could support a near-term rally, the medium-term technicals and fundamentals of the PMs are deeply bearish. Therefore, investor optimism should turn to pessimism in the coming months.

Do you want free follow-ups to the previous article and details that are not available to more than 99% of investors? Sign up for our free newsletter today!

Reference-www.fxstreet.com