-

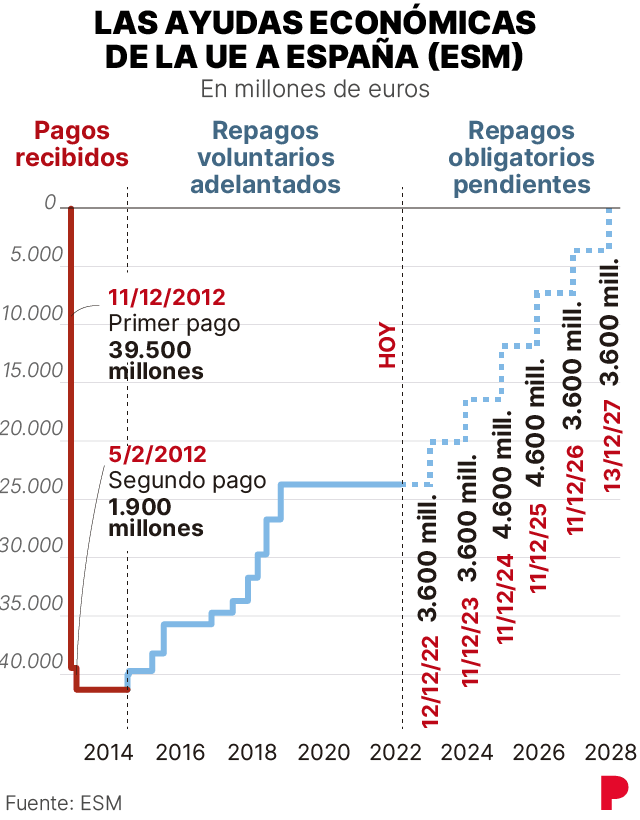

The Treasury must reimburse 27,721 million to the MEDE between 2022 and 2027, after having repaid voluntarily and in advance 17,612 million until 2018

-

The payment is manageable except for drastic deterioration in financing conditions, but it hinders the consolidation of public finances

Spain has started to receive the 69,528 million euros in non-refundable aid assigned by the European Union until 2023 to modernize its economy and get out of the coronavirus crisis, like the rest of the community partners. But unlike the vast majority of these, the country must also pay to the EU multi-million dollar amounts as of next year and until 2027. Specific, 27,721.46 million, the equivalent of 39.9% of grants you will receive. Thus, twelve months from now, the December 11, 2022, the Treasury will have to face the mandatory first payment of rescue received in the previous crisis to restructure the financial sector and save bankrupt savings banks, just a decade after having received it.

Spain was at the edge of the abyss in that 2012. Among rumors of a possible euro break and growing international doubts on the real situation of Spanish banks after the bursting of the real estate bubble, the treasure did not lose its ability to finance an investment in the markets public deficit skyrocketed to 10% of GDP, but investors were increasingly demanding a few higher interest for lending you money. Even if it could have continued to issue debt, this rise in cost would have led to public finances to be unsustainable, with the consequent suspension of payments by the State, so the Government of Mariano Rajoy He was forced to ask for help to the rest of the EU countries in June 2012.

After tough negotiations and in exchange for a demanding list of reforms enshrined in a Memorandum of Understanding (known as MoU) and supervised by the men in black from the ‘troika’, community partners approved a funding line of up to 100,000 million of euros in more favorable conditions than those that Spain could obtain in the market. Finally alone 41,333 million were used, which were destined to rescue BFA-Bankia, Catalunya Caixa, Nova Caixa Galicia, Banco de Valencia, BMN, Ceiss, Caja 3 and Liberbank (today all disappeared after joining other entities), as well as to finance the creation of the Sareb, the bad bank that received the toxic real estate assets from these savings banks and that still causes headaches for the State.

Advance and pending payments

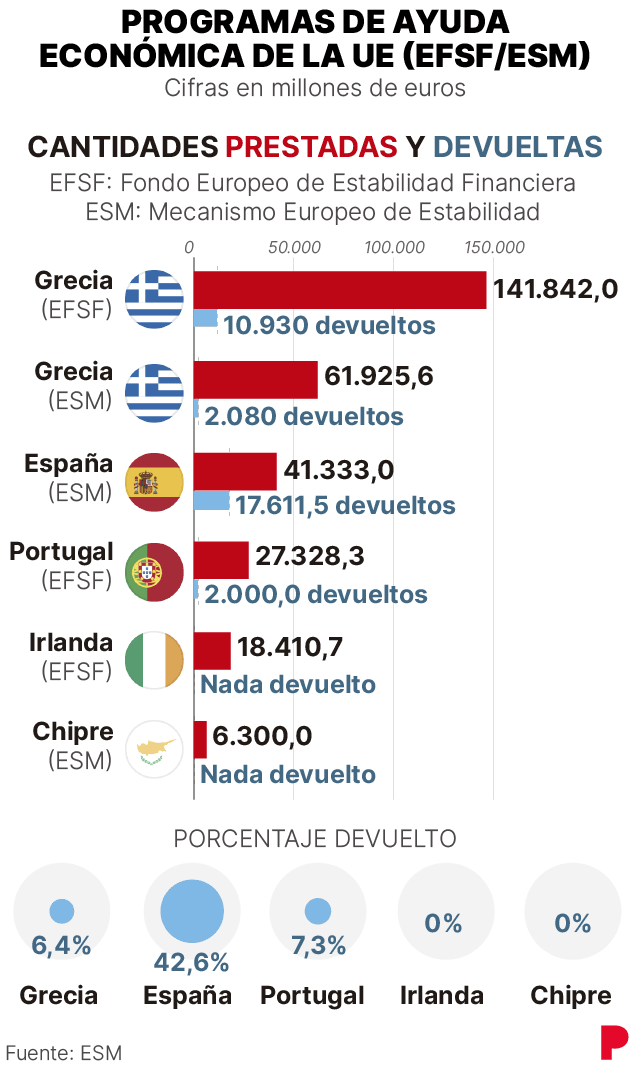

The figure that is still pending to be returned is lower than that received because Spain repaid to the European Stability Mechanism (ESM) 17,612 million euros, 42.6% of what is perceived, in a way voluntary and anticipated in nine installments between July 2014 and October 2018. It was about giving an image of strength and speedy recovery: it was the first country of the five rescued (they were also Ireland, Portugal, Greece and Cyprus) to begin repaying your debt and, by far, is the one that has paid the highest percentage to date.

As for the amounts still pending, it seems very manageable for Spain, except one radical deterioration of the financing conditions that are unlikely today given the monetary policy plans of the Banco Central Europea (ECB) despite rising inflation. On the one hand, the payments are escalated in the next six years (3,600 million in 2022, 2023, 2026 and 2027 and 4,600 million in 2024 and 2025). On the other, they are relatively small: to put them in perspective, the 3.6 billion for next year is hardly a 2.2% of the 162,846 million that the Treasury plans to issue in 2022 to pay off previous debts.

Third, the state is financing some historically low interest thanks to the ECB’s bond purchases. The average cost of outstanding debt is 1.63%, compared to 4% in 2012, and the cost of debt new issues has been this year in a -0.02% average. Even as rates start to rise because of the impending reduction in central bank purchases, maturing debt has rates so high that it will still be much cheaper to replace it, thus reducing the average cost of outstanding debt. At the end of January, for example, about 23,000 million euros of a 10-year obligation with a coupon of 5.85% mature. “The Treasure is prepared for the normalization of monetary policy by the ECB “, recently assured in Congress its secretary general, Carlos Body.

Balance

Related news

The European rescue, in any case, has been financially favorable for Spain. According to the MEDE, the State paid him 1,053.37 million from euros to commissions Y 1,634.15 million in interest between 2013 and 2020 (the rate has fluctuated from the initial 0.5% to go up to 1.1% in 2017 and then down to 0.8% last September). But, highlights the community rescue fund, Spain is saved around 1.2 GDP points in interest until 2019 (about 12 billion euros) compared to what it would have cost him to get the money in the market in December 2012. In addition, the agency adds, the bank restructuring that it allowed is one of the fundamental causes of the country’s economic recovery as of 2014.

On the other side of the scale, but not attributable to the rescue itself, is that the overwhelmingly of the money injected has been lost forever or its recovery is more than doubtful. Thus, of the 24,096 million euros contributed to Bankia, they were considered recoverable 5,974 million at the end of 2020, which will foreseeably fall this year by an additional more than 1,000 million after its absorption by Caixabank; the 2,192 million injected into the Sareb have already been accounted for lost; and of the 32,610 million with which the rest of the entities were rescued, they lost 28,133 million, 86.2%. If it had not been volatilized, all that money would have made the bill with the ESM much more comfortable for the coming years and would have facilitated the consolidation of public finances after the record of debt caused by the pandemic.

Reference-www.elperiodico.com