Rising interest rates tend not to be good news for most people, especially Canadians who have taken on a lot of debt to buy a home in the country’s red-hot real estate markets in recent years.

The latest rate hike is expected to come on Wednesday and the central bank is expected to raise its key interest rate by as much as 75 basis points to combat runaway inflation.

There’s a good reason that might sound scary to many people, especially those who recently bought a home with an adjustable-rate mortgage.

According to a report released this week by the Canada Mortgage and Housing Corporation (CMHC), more than half of all mortgages taken out in the second half of 2021 were adjustable-rate mortgages, an anomaly not seen in the last 10 years in a country where people tend to strongly favor fixed rates.

Fueled by deep discounts on variable rates, that trend also continued through the first two months of 2022, with more than 55 percent of mortgages taken out at variable rates.

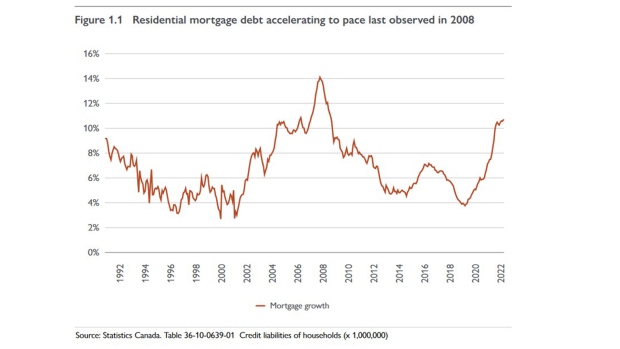

In addition, mortgage growth in the last 12 months increased to a level not seen since 2008, according to CMHC.

“So when we look at 2021, and even early 2022, mortgage debt has not only increased, but actually accelerated. So we are talking about a close to 10 percent increase in mortgage debt compared to the previous year,” Tania Bourassa-Ochoa, senior economist at CMHC, told CP24.com in an interview. “So Canadians have high levels of indebtedness, and that’s something that we’ve been monitoring very closely.

Obviously, it is a potential source of vulnerability for the housing system. So it’s definitely something we’re watching very closely.”

Bourassa-Ochoa said the mortgages that have been taken out are also larger as people spend more to keep up with rising home prices.

MORTGAGES LAST PLACE CANADIANS WANT TO SLIP

She said those with adjustable-rate mortgages will be the first to feel the pressure when rates go up, but added “there are still some nuances” to the situation.

For example, those who have chosen to regularly pay more than the minimum each month may not notice an increase in their payments, even though they will pay less principal each month than before.

Mortgage delinquencies, the proportion of mortgage holders who have missed their payments for 90 days or more, are also at record lows.

While Bourassa-Ochoa acknowledged that mortgage delinquencies are a “late indicator” of debt problems, she said mortgages likely aren’t the first place debt problems arise.

“So I think in the next few months, in the next few quarters, it’s going to be interesting to look at delinquencies on other credit products, like credit cards, auto loans, personal loans.”

Those, he said, will likely be early indicators if Canadians start to feel the pressure of rising interest rates.

“Usually those are the loans that are going to be in default first, if I could put it that way. So that could be an early indication before mortgage payments,” she said. “Canadians will try to do everything they can to make their mortgage payments on time.”

The latest CMHC report also notes that the recent acceleration in home lending was due to the rise in unsecured mortgages for both home purchases and refinancing. That’s important because it indicates that most of the new debt is being taken out by people who aren’t over-leveraged (mortgage insurance is required if you put down less than 20 percent of a property’s purchase price).

And while the acceleration in borrowing is at the highest level since 2008, when the US subprime crisis triggered a recession, Bourassa-Ochoa notes that “a variety of different measures and tools were put in place ” to ensure stability. in the Canadian housing system.

She points to a “stress test” put in place for borrowers in 2018 to ensure they can withstand an additional two percent increase in rates. Canada also has full recourse lending, which means lenders can repossess assets in default if a home sale doesn’t cover the debt, making it less attractive for borrowers to leave their homes if they get into trouble. problems.

And despite the recent craze for variable rates, Bourassa-Ochoa points out that most mortgages in Canada are still five-year fixed products, and therefore borrowers will only face higher rates when it comes time to renew. .

That sentiment is shared by RBC chief economist Nathan Janzen.

Speaking to CP24 this week, he said the expected rate hike on Wednesday would take the bank’s overnight rate to just 2.25 percent, still a historically low rate.

“We expect more hikes to come. We have another 100 basis points over the next two meetings to get to an overnight (advance) rate of 3.25 percent, so it will flow through to household borrowing costs,” Janzen said. “Some variable rate mortgage payments reset immediately, effectively once the Bank of Canada changes interest rates, but for many other mortgage holders it takes time. They only reset when you need to renew. That’s another reason why we expect the impact on household purchasing power to be delayed and see a bigger impact in 2023.”

RBC, the country’s largest mortgage lender, forecasts a mild recession by 2023, along with a 10 percent drop in house prices in the next year.

This week, the Toronto Regional Real Estate Board said June sales fell 41 percent compared to the same month a year earlier, indicating that rising rates and uncertainty about the economy may already be cooling real estate markets.

‘THE MILLION DOLLAR QUESTION’

Mortgage brokers are definitely recording some of that anxiety from potential clients.

“I guess the million-dollar question we get asked right away, early on, is where are interest rates going,” said Anthony Contento, owner and broker at Sherwood Mortgage Group of Toronto.

“If we all knew that, if we had that crystal ball, we would all be millionaires”,

He said there is “a lot of uncertainty” when potential borrowers come to him these days.

“There is a lot of uncertainty about whether or not they should insure it or use the variable rate. So I think the consumer is a little bit intimidated by one and two, really unsure where to go,” he says. “The reality is that a lot of them are renewing whatever the banks are offering them because if they want to go somewhere else, they need to qualify again.”

He said that even at historically low interest rates, the stress test makes it difficult for some people who are renewing to requalify with new lenders.

“For sure there is a panic button right now that many are pressing not knowing where to go,” he said. “And there are a lot of people right now who are coming to maturity where they once paid 2.2 or 1.9 on a fixed rate three or four years ago and now they know they’re looking at 4.99. That certainly changes the whole picture as far as what they can afford.

“So it’s certainly a little gray cloud right now hanging over the consumer, and their decision about what they should be doing.”

He noted that adjustable rate mortgages may still be attractive to many people who are willing to put up with a few increases for a discounted rate, but said ultimately everyone needs to make a clear assessment of their own financial picture before deciding what to do. works better for them.

“The wisest thing would probably be to sit down with your partner or, if you’re alone, and go through your entire budget and where you are,” says Contento. “It will give you a better indication of what your comfort level is going to be, where your risks are in terms of whether you want to play that variable game or stay fixed. Once you’ve worked and drawn that line on paper and the pros and cons of a fixed or variable, I think only the consumer himself knows what he can afford.”

The message from Contento and other lenders at the moment is to do your homework before you take out a loan or refinance and make sure it fits your financial goals, even if rates continue to rise a bit.

“We know that buying a home is one of the biggest purchases Canadians will make. So it’s very important that you do your research,” says Andrea Metrick, Senior Director of Home Equity Financing at RBC. “It’s really important to look for the right tools, to have the right conversations about buying a home right now or knowing when you’re thinking about buying a home how that fits into your overall financial plan.”

She said homeowners need to think about the one-time costs, ongoing costs and potential emergency costs associated with home ownership when making a buying and lending decision.

“Homeowners or potential homeowners need to really think about, you know, what are the trade-offs that I might need to make with the factors that I need to consider and now is the right time to shop within those factors for my personal situation.”

While it’s hard to predict exactly what will happen beyond the next two quarters, Bourassa-Ochoa said the industry and government will be watching closely.

“You know, what we’re really watching closely is definitely the level of indebtedness.

“In the context of rising and rapidly rising interest rates, yes, inevitably, that will put some pressure on some households and especially households that are more in debt.”